Google profits from ads promoting ‘instant’ money and loans delivered ‘faster than pizza’ despite pledging to protect users from ‘deceptive and harmful’ financial products. The adverts were shown to people in the UK who searched for terms such as “quick money now” and “need financial help” and directed users to companies offering high interest loans. […]]]>

Google profits from ads promoting ‘instant’ money and loans delivered ‘faster than pizza’ despite pledging to protect users from ‘deceptive and harmful’ financial products. The adverts were shown to people in the UK who searched for terms such as “quick money now” and “need financial help” and directed users to companies offering high interest loans. […]]]>Google profits from ads promoting ‘instant’ money and loans delivered ‘faster than pizza’ despite pledging to protect users from ‘deceptive and harmful’ financial products.

The adverts were shown to people in the UK who searched for terms such as “quick money now” and “need financial help” and directed users to companies offering high interest loans.

One, listed in Google search results above links to the government website and debt charities, promised “guaranteed money in ten minutes” for people with “very bad credit”.

The Advertising Standards Authority said last night it was assessing 24 adverts identified by the Observerpaid for by 12 advertisers, including loan companies and credit brokers as well as suspected scammers.

The regulator said many of the promotions were likely to breach rules on socially responsible advertising which state that advertisements must not “trivialize” loan underwriting. “A disproportionate emphasis on speed and ease of access to interest rates is likely to be considered problematic,” according to its guidelines.

Google said the ads flagged with it violated its policies and had been removed. He previously pledged to fight “predatory” loan promotions, banning ads for payday and high-interest loans in 2016.

The promotions appeared to clearly violate its policy, explicitly referring to “payday loans” and linking to websites offering ultra-high interest rates of up to 1,721%. Many ads removed by Google on Friday had been replaced by similar promotions within hours, some from the same advertisers reported by the Observer.

It comes amid a growing cost of living crisis, described by the Institute for Fiscal Studies as the worst financial crisis in 60 years.

Households are battling rising prices on multiple fronts, including rising energy bills, grocery costs, and gasoline and diesel prices, compounded by supply chain disruptions and issues caused by the pandemic, Brexit and the war in Ukraine.

Charities and debt campaigners have said such loans could trap people in financial difficulty, who may impulsively apply and find themselves “trapped in a spiral”.

Adam Butler, head of policy at debt charity StepChange, said financially vulnerable people were most likely to be drawn in “due to a complete lack of borrowing alternatives”. “The repeated use of these types of products to make ends meet – often the reason people turn to this type of borrowing – can trap people in a spiral that is very difficult to get out of,” a- he declared. “With the cost of living crisis set to worsen further in the coming months, there is every chance that we will see an increase in the number of people forced to turn to this type of borrowing just to s ‘get out.”

Many promotions appeared to be deliberately aimed at people in financial difficulty, with messages such as “bad credit, welcome”. They suggested there would be little review with messages such as “no credit check” and “no call”.

An ad read: “Instant payday loans paid in 10 minutes. Bad credit OK, irrelevant credit history. Another company described the loans available as suitable for “small emergencies”.

Another website, Tendo Loan – one of the most prolific advertisers – claimed to offer: “Cash in 10 minutes guaranteed. 3-36 months. No credit checks! It added: “A loan delivered faster than pizza! 2 minutes to apply and 10 minutes to deposit to your account. Apply 24/7. Tendo Loan did not respond to requests for comment.

The Financial Conduct Authority said adverts suggesting the loans were ‘secured’ or involved ‘no credit checks’ were misleading. He said companies should not make ‘false’ claims, such as suggesting that credit is available regardless of a customer’s financial situation or status, and could be subject to action of execution.

In some cases, the advertisements appeared to be linked to fraudulent websites, redirecting users to websites where they entered their personal information, including banking information, phone number, date of birth and address.

Yvonne Fovargue, chair of the all-party caucus on debt and personal finance, described the ads as “online harm” and called on Google and the government to tackle them.

“It’s an obvious targeting ploy for people on the edge who, instead of taking out a loan, should seek debt advice,” she said.

The ASA has previously ruled against payday lenders and said it is evaluating evidence of potential violations.

He added that while “the responsibility ultimately rests with the advertiser”, media platforms such as Google “also have some responsibility to ensure that content complies with the rules”. “Platforms should and are taking steps to ensure misleading and irresponsible ads are not posted,” a spokesperson said.

Google said, “We have strict advertising policies in place for financial services products and prohibit ads for payday loans. We have a dedicated team working to protect users from malicious actors trying to evade detection. In 2020, we blocked or removed over 123 million ads for violating our financial services policies. »

Stella Creasy, anti-payday lending campaigner and Labor MP for Walthamstow, described companies offering super-high-interest short-term loans as ‘legal loan sharks’ who seek to ‘exploit’ people’s financial difficulties. “We need the government and regulators to remain constantly vigilant and act to stop these companies before they make a bad situation worse for so many people,” she said.

MoneyMutual is a payday loan company that lets you borrow from $200 to $5,000 in as little as 24 hours. By filling out a simple form on MoneyMutualyou can instantly connect to 91 lenders to find the best deal in your area. Is MoneyMutual legit? How does Money Mutual work? Keep reading to find out […]]]>

MoneyMutual is a payday loan company that lets you borrow from $200 to $5,000 in as little as 24 hours. By filling out a simple form on MoneyMutualyou can instantly connect to 91 lenders to find the best deal in your area. Is MoneyMutual legit? How does Money Mutual work? Keep reading to find out […]]]>MoneyMutual is a payday loan company that lets you borrow from $200 to $5,000 in as little as 24 hours.

By filling out a simple form on MoneyMutualyou can instantly connect to 91 lenders to find the best deal in your area.

Is MoneyMutual legit? How does Money Mutual work? Keep reading to find out everything you need to know about this payday loan website.

What is MoneyMutual?

MoneyMutual, available online at MoneyMutual.com, is a payday loan website that lets you get anywhere from $200 to $5,000 deposited into your account within 24 hours.

Simply complete the form on MoneyMutual.com to get started and you can instantly see offers from lenders serving your area.

MoneyMutual is one of the most trusted payday loan websites available online today. With over 2,000,000 customers to date, MoneyMutual has a proven track record of providing customers with the payday loans they need. You can see MoneyMutual commercials on TV, and TV’s Montel Williams was a spokesperson for MoneyMutual for almost a decade.

How does MoneyMutual work?

MoneyMutual makes it easy to get a short term loan in 24 hours or less and is easily one of the best bad credit loan providers of 2022.

As long as you’re 18, have at least $800 a month of verifiable income, and have a checking account, you should be able to find a payday loan through MoneyMutual.

Simply enter your information into MoneyMutual.com, then view payday lender offers. MoneyMutual partners with over 90 companies to ensure customers can get the payday loans they need when they need them.

After choosing the offer via MoneyMutual’s online comparison screenyou visit the lender’s website, fill in additional information and get the money you need as soon as possible.

Here’s how it works:

- Step 1) Provide your information: Fill out the form on MoneyMutual.com and MoneyMutual sends your information to the lenders.

- Step 2) Lender Review: Lenders verify your information instantly to determine the right person. Then they show you their best offer on the next page.

- Step 3) Get your money: Browse a list of loan offers and get funds deposited into your bank account in as little as 24 hours.

You can use MoneyMutual for loans ranging from $200 to $5,000.

How much does Money Mutual cost?

MoneyMutual is available for free. You fill out the form and submit your information for free via the online marketplace.

However, once you choose a lender through MoneyMutual, that lender charges a fee in exchange for lending money. Read the terms carefully to make sure you understand how much it costs to borrow.

How long does it take to use MoneyMutual?

It takes about five minutes to complete the MoneyMutual online form. If you have used MoneyMutual before and are a loyal customer, it takes even less time.

Once you fill in the online form and select an offer, you can get the money in your account in just 24 hours.

How do MoneyMutual lenders work?

MoneyMutual works with over 90 lenders to find the best deal for your unique needs. Each lender considers your personal information and financial data provided by you to ensure an optimal match.

Here’s how lenders look at your information, according to MoneyMutual:

- Lenders automatically review your information after you submit an application through the website

- Each lender follows the previously established requirements to make a decision

- If a lender decides that they want to lend you money, you will be redirected to their website, where you can review the terms of the loan and accept the loan.

- Lenders may also contact you to verify your personal information, confirm your bank account number and finalize the loan.

That’s it. Like other payday lenders, payday lenders with MoneyMutual are legally required to disclose all fees up front. The law also prevents them from charging excessive annual interest rates. Check all fees and charges in advance to avoid any surprises.

What’s the catch?

There is no “trap” in using MoneyMutual. The website genuinely connects you with payday lenders and short-term lenders in your area who can lend you money as quickly as possible.

Be sure to read the terms and conditions on your lender’s website to make sure you understand the terms of the contract. Although MoneyMutual is a free service, each lender has its own terms and conditions.

MoneyMutual Reviews: What Customers Are Saying

The payday loan industry is filled with shady companies. However, MoneyMutual is one of the best known and oldest companies in the industry. With celebrity endorsements from Montel Williams and over a decade of experience, MoneyMutual has helped over 2 million people access the money they need.

Here are some of the MoneyMutual reviews from verified customers online:

Most customers agree that MoneyMutual works as advertised to provide them with sources of short-term funding, bringing borrowers and lenders together in a transparent marketplace.

Customers love MoneyMutual because of the transparent rates and lending system, which makes it easy to see the best deal from each lender

Many use MoneyMutual after seeing the advertisements on television, finding that MoneyMutual lives up to its claims of providing efficient loans to people in need.

Some customers even praise MoneyMutual’s customer service, which is not the strong point of most payday loan companies.

Negative reviews tend to leave bad reviews because of bad interactions with the third-party lender, not because of bad interactions with MoneyMutual; some lenders have high interest rates and fees, for example, which may surprise customers who don’t read the terms and conditions

MoneyMutual Requirements

To borrow money through MoneyMutualyou must meet the following conditions:

- Be at least 18 years old

- Have at least $800 per month of verifiable income

- Have a checking account

Some lenders require additional items from borrowers, such as an SSN. Others, however, require no additional information or data.

About MoneyMutual

MoneyMutual is a free online resource based in Las Vegas, Nevada. The company is not a lender: it partners with lenders to help people find payday loans for their short-term financial needs.

Between 2010 and 2018, Montel Williams was the spokesperson for MoneyMutual.

You can contact MoneyMutual via:

- E-mail: [email protected]

- Call:

844-276-2063

Last word

40% of Americans would not be able to come up with $400 in an emergency, according to the Economic Well-Being of US Households report.

To get a fast, easy and affordable payday loan from a trusted lender, visit MoneyMutual.com today. The website connects you with dozens of lenders in your area to ensure you get the best deal, and you can get $200 to $5,000 deposited into your account in as little as 24 hours.

To learn more about MoneyMutual or to apply online today, visit the official website at MoneyMutual.com.

Affiliate Disclosure:

Links in this product review may result in a small commission if you choose to purchase the recommended product at no additional cost to you. This serves to support our research and writing team. Know that we only recommend high quality products.

Warning:

Please understand that any advice or guidance revealed here does not even remotely replace sound medical or financial advice from a licensed healthcare provider or certified financial advisor. Be sure to consult a professional doctor or financial advisor before making any purchasing decisions if you are using any medications or have any concerns from the review details shared above. Individual results may vary as statements regarding these products have not been evaluated by the Food and Drug Administration or Health Canada. The effectiveness of these products has not been confirmed by the FDA or Health Canada approved research. These products are not intended to diagnose, treat, cure, or prevent any disease or to provide any type of enrichment program.

Gallery

The news and editorial team at Sound Publishing, Inc. played no role in the preparation of this post. The views and opinions expressed in this sponsored post are those of the advertiser and do not reflect those of Sound Publishing, Inc.

Sound Publishing, Inc. accepts no responsibility for any loss or damage caused by the use of any product, and we do not endorse any product displayed on our Marketplace.

]]> Most of the time, people get a payday loan because they can’t get quick financing anywhere else. Unfortunately, the financial situation can worsen if the borrower is unable to repay what he owes. Depending on how long it’s been since you received the loan, the lender could threaten to take legal action against you and […]]]>

Most of the time, people get a payday loan because they can’t get quick financing anywhere else. Unfortunately, the financial situation can worsen if the borrower is unable to repay what he owes. Depending on how long it’s been since you received the loan, the lender could threaten to take legal action against you and […]]]>Most of the time, people get a payday loan because they can’t get quick financing anywhere else. Unfortunately, the financial situation can worsen if the borrower is unable to repay what he owes.

Depending on how long it’s been since you received the loan, the lender could threaten to take legal action against you and garnish your wages. Borrowers in this situation have options that could potentially help them.

What can happen if you don’t repay a payday loan

While every situation may have differences, there are typical consequences when you don’t repay a payday loan on time.

Withdrawals from your bank account

Most lenders repeatedly attempt to withdraw the funds from your bank account, as permitted by the terms of the loan agreement. If transactions are declined by your bank due to insufficient funds, the lender may initiate withdrawals for lower amounts.

Even if the lender collects some of the outstanding balance using this method, you could still face financial hardship if further banking transactions are declined. Plus, bank charges could add up and cost you several hundred dollars in a short period of time.

Collection agencies get involved

You can expect the lender to initiate collection efforts, including repeated calls and letters demanding payment, while continually trying to write your account. The lender could also sell your debt to a collection agency or hire a lawyer to collect what is owed to you.

You may be able to stop collection actions by asking the lender for an extension. Some states have laws that require payday lenders to grant extended payment plans to borrowers upon request. Remember that these extensions often come with additional fees and interest.

Declining credit score

The lender could also report the delinquent account to the credit bureaus once it is turned over to a collection agency. Your credit score will likely drop and the negative mark will remain on your credit report for up to seven years. Therefore, you may find it difficult to obtain competitive financing offers in the future.

You can take steps to start rebuilding your credit score after defaulting on a payday loan. First, review your credit report to identify any other delinquent accounts and update it, as payment history is the most important part of your credit score. You also want to find errors and challenge them quickly.

Also adjust your spending plan to free up funds that you can use to start paying off credit card debt in the near future. You want to do this to lower your credit utilization rate, or the amount of revolving credit you use, because it makes up 30% of your credit score.

Most importantly, keep an eye on your credit report and build responsible debt management habits over time to give your credit score the best chance of getting stronger over time.

Negotiations with the lender

It’s much cheaper for the lender to collect than to sue you, and selling the balance to a debt collector for pennies on the dollar means the lender will only get a small percentage of what’s owed to them. .

Both circumstances give you the leverage to eventually settle payday loan debt for a fraction of the outstanding balance. Offer an amount you can afford to pay in one lump sum and mention your intention to file for bankruptcy if the lender won’t budge. The lender may be willing to compromise with you since bankruptcy means they may not be able to collect.

Lender lawsuit

If the lender takes you to court, the onus is on them to prove that you owe the debt. Simply ask that they provide the documentation or agreement you signed when taking out the loan. If the debt collector cannot provide this information, the judge will likely dismiss the case. But if the lender proves that you are indebted and obtains a judgment from the courts, you could be ordered to pay or have your wages garnished.

Quick note: If the lender is threatening to throw you in jail, quickly contact your state attorney general’s office to file a complaint.

How to get the money to pay off a payday loan

Instead of ignoring a delinquent payday loan and ruining your credit, consider these options for paying off debt:

- Apply for a peer-to-peer lending. If your credit score is low, a peer-to-peer loan is worth considering. You will find these loan products in online lending marketplaces that connect potential borrowers with investors looking to lend you funds in exchange for a return. You can usually compare multiple loans with one application, and you’ll usually need to provide proof of income or assets to be approved.

- Obtain a debt consolidation loan. A debt consolidation loan allows you to combine high-interest debt into a single loan product with a lower interest rate. Most debt consolidation loans have a fixed interest rate and you will make equal monthly payments over a set period. The most competitive loan terms are reserved for borrowers with good or excellent credit. Even with less than optimal credit scores, your rate could be lower than what you received with the payday loan.

- Consider a short-term emergency loan. Credit unions and some community banks typically offer short-term emergency loans as alternatives to payday loans. They are usually available with slightly lower interest rates and for small dollar amounts, capped at $1,000, and may not require a credit check for approval.

- Register in a debt management plan (DMP). It should be used as a last resort if you have exhausted all your options. DMPs are available through non-profit agencies. A credit counselor will contact the payday lender on your behalf to negotiate a modified repayment plan that suits your budget. You’ll pay the loan principal balance in full, but the downside is that signing up for a DMP could cause other creditors to close your credit card accounts, causing further credit damage.

You can also try talking to friends and family or looking for ways to adjust your finances to cover expenses such as temporarily canceling streaming subscriptions, switching to a lower food budget.

When you’re low on cash between paychecks or have an unexpected financial emergency, a payday loan can be a tempting option to help you make ends meet or access cash quickly. However, these short-term loans, which are usually due on the day of your next payday, are extremely risky. They come with very high interest […]]]>

When you’re low on cash between paychecks or have an unexpected financial emergency, a payday loan can be a tempting option to help you make ends meet or access cash quickly. However, these short-term loans, which are usually due on the day of your next payday, are extremely risky. They come with very high interest […]]]>When you’re low on cash between paychecks or have an unexpected financial emergency, a payday loan can be a tempting option to help you make ends meet or access cash quickly. However, these short-term loans, which are usually due on the day of your next payday, are extremely risky. They come with very high interest rates and other charges. The interest rate on payday loans in the United States ranges from 154% to 664% or more.

Equally troubling, payday loans are often marketed to those who can least afford them, i.e. people who earn less than $40,000 a year. Although this type of loan is marketed as a short-term loan, payday loans can create a cycle of debt that is difficult to break free from.

What is a personal loan?

A payday loan is usually a short-term loan, lasting two to four weeks, that does not require collateral to be obtained. These types of loans are generally supposed to be repaid in a single payment with your next paycheck, when you receive Social Security income, or when you receive a pension payment.

In the majority of cases, payday loans are granted for relatively small amounts, often $500 or less, with the average borrower getting a payday loan of around $375. In some cases, payday loans can be made for larger amounts.

To obtain a payday loan, borrowers are asked to write a personal check for the amount of debt plus finance charges and fees. If the loan is not repaid on time, the lender will deposit the check to recover their funds. Some lenders may request authorization to electronically deduct the funds from your bank account instead of requiring you to provide a personal check.

Payday loans generally do not involve credit checks, and your ability to repay debt while continuing to pay your daily expenses is generally not considered part of the application process.

Who usually takes out a personal loan?

Payday loans are most often sought out by those with ongoing cash flow issues, as opposed to borrowers who find themselves facing a financial emergency. A study of payday loans conducted by Pew Charitable Trusts found that the vast majority of payday loan users, 69%, first took out this type of loan to cover recurring expenses such as utility bills. utilities, rent, mortgages, student loan payments or credit cards. bills. Only 16% of borrowers use payday loans for unexpected expenses.

These types of loans are also widely used by people living in neighborhoods and communities that are underserved by traditional banks or by those who do not have a bank account with a major financial institution. There are approximately 23,000 payday lenders across the country, many of which are located in storefronts or operate online.

What are the risks of personal loans?

Due to the many risks associated with payday loans, they are often considered predatory loans.

For starters, payday loans often come with astronomical interest rates. Those who take out such loans have to pay between $10 and $30 for every $100 borrowed. A typical payday loan with a two-week repayment term and a fee of $15 per $100 equates to an APR of nearly 400%.

Many payday lenders also offer rollovers or renewals, which allow you to simply pay the cost of borrowing the money on the loan’s due date and extend the balance owing for a longer period. It can be a slippery slope that has borrowers quickly getting in over their heads with accrued fees and interest. According to the Consumer Financial Protection Bureau, borrowers default on up to one in five payday loans.

Further, since payday loans do not consider the full financial situation of the applicant, including their ability to meet other financial obligations and living expenses while repaying the payday loan, this type of loan often leaves borrowers in a vicious cycle of debt.

Are payday loans really worth it?

With their high interest rates and fees, a payday loan is rarely a good idea. The fees alone cost Americans $4 billion a year. Because the costs associated with these loans are so high, borrowers often struggle to repay them and take on more debt, so it’s a good idea to carefully consider your options before taking out a payday loan.

However, if you are in dire need or need cash quickly and you are absolutely certain that you can repay the loan with your next paycheck, a payday loan may be a good idea. These loans may also be worth considering if you have no other financial options or have poor credit and would not qualify for a traditional loan.

Alternatives to payday loans

Before taking on the significant financial risks associated with a payday loan, consider other alternatives that may be less expensive. Some of the options to consider include:

- Personal loan: For those with good credit, a personal loan can be a safer and more cost-effective borrowing option. Plus, if you need cash fast, there are online lenders who can provide personal loan funds in as little as a day or two.

- Borrowing money from family or friends: Payday loans should be a last resort. If you have family or friends who are willing to help you, it may be better to borrow money from loved ones than from a predatory lender.

- Home Equity Loan: Tapping into the equity in your home will give you a much more competitive interest rate than a payday loan. Home equity loans are a popular way to access cash to consolidate debt or pay for other large or unexpected expenses. However, to access the equity in your home, you will need to meet certain requirements, including having a good credit rating, a stable income, and a debt-to-equity ratio of 43% or less.

A ballot initiative to restrict interest rates charged by payday lenders has removed one final procedural hurdle, with supporters set to collect signatures that could put it on the ballot in November. On Friday, the Michigan Board of State Solicitors approved petition language for the Michiganders for Fair Loans ballot initiative. As noted in the […]]]>

A ballot initiative to restrict interest rates charged by payday lenders has removed one final procedural hurdle, with supporters set to collect signatures that could put it on the ballot in November. On Friday, the Michigan Board of State Solicitors approved petition language for the Michiganders for Fair Loans ballot initiative. As noted in the […]]]>A ballot initiative to restrict interest rates charged by payday lenders has removed one final procedural hurdle, with supporters set to collect signatures that could put it on the ballot in November.

On Friday, the Michigan Board of State Solicitors approved petition language for the Michiganders for Fair Loans ballot initiative. As noted in the petition, the proposal would cap the annual percentage rate (APR) on payday loans at 36% and empower Michigan’s attorney general to sue lenders who exceed that rate. The group says payday lenders are currently allowed to charge “interest rates and fees equivalent to an annual percentage rate of 340% or more.”

Campaign spokesman Josh Hovey called the charging of these rates “outrageous” and said that with the canvassers’ approval, they will soon begin collecting petitions to reform this “predatory lending practice”. The group says its initiative is modeled on similar legislation in 19 other states, including Nebraska, which capped payday loan rates at 36% APR in 2020. with almost 83% support.

However, business interest groups say the measure will not provide protection against predatory payday lending, but rather penalize lenders who play by the rules.

Fred Wszolek is a Republican strategist and co-founder of Lansing-based Strategy Works. In an interview with Michigan advance On Friday, he said the initiative “effectively bans the industry under the guise of a proposal that simply caps the interest rate.”

Wszolek says the industry is already tightly regulated and called APR a “dumb statistic” to use as a metric.

“It’s a great kind of apple-to-apple comparison of this 30-year loan to this 30-year loan, but when you’re talking about a two-week loan, to translate the interest rate and the fees into a rate annual percentage, that’s a stupid math,” he said. “I mean, it’s just a meaningless number. If you think of the bad check fee as a one-week loan for you because they covered your check, then the APR on the $25 NSF check fee is about 1,200%.

Wszolek says that due to the short-term nature of payday loans, limiting the APR to 36% will not provide the profit margin needed for these lenders to operate their storefronts, meet mandatory compliance regulations and write off numbers. loans that will inevitably go unpaid.

He also says that if the initiative is approved, it will only affect state-regulated operations, not overseas-based online lenders or tribal-owned payday lenders.

Fred Wszolek is a Republican strategist and co-founder of Lansing-based Strategy Works. In an interview with Michigan Advance on Friday, he said the initiative “effectively bans the industry under the guise of a proposal that simply caps the interest rate.”

“I mean, they’re not getting rid of the regulation of this industry, from a consumer perspective, because the consumer can’t tell the difference between all the websites. I mean, you can’t say you’re dealing with a tribe-run payday loan operation. That’s beyond the reach of Michigan law. You can’t say you’re really dealing with a company that’s in the Netherlands Antilles” or has a “PO box somewhere in the Caribbean”.

Hovey responded to those criticisms in an interview Friday with the Michigan Advance, acknowledging that while the ballot proposal only applies to state-licensed lenders, the fees charged by those lenders are equivalent to three-digit interest rates.

“I can’t imagine the average Michigander would consider a 300% interest rate ‘legitimate’ or just because legitimate lenders don’t do that stuff,” Hovey said.

As for concerns that small dollar loans won’t be available, he says there are credit unions that offer payday loan alternatives.

“The President of Isabella Community Credit Union even testified before the House Regulatory Reform Committee this week that they are able to offer small loans in as little as 15 minutes that have a maximum APR of 23 % that can be repaid over 11 months. period,” Hovey said.

Groups supporting the ballot initiative include the Michigan League for Public Policy, Habitat for Humanity of Michigan, and the Michigan Association of United Ways. Sandra Pearson, president of Habitat for Humanity Michigan, formerly told the Associated Press that even though payday lenders offer short-term loans as a quick fix, they often leave borrowers in worse financial shape than before.

Michiganders for Fair Lending expects to begin collecting the 340,047 valid signatures required to place the measure on the November ballot within the next two weeks.

Get morning headlines delivered to your inbox

Kevin Stent / Stuff Nicola Willis is calling on the government to pass legislation to quickly address the unintended consequences of new responsible lending regulations. National has drafted legislation it says could undo the damage new responsible lending regulations have done to borrowers’ chances of getting a home loan. National Housing spokeswoman Nicola Willis said […]]]>

Kevin Stent / Stuff Nicola Willis is calling on the government to pass legislation to quickly address the unintended consequences of new responsible lending regulations. National has drafted legislation it says could undo the damage new responsible lending regulations have done to borrowers’ chances of getting a home loan. National Housing spokeswoman Nicola Willis said […]]]>Kevin Stent / Stuff

Nicola Willis is calling on the government to pass legislation to quickly address the unintended consequences of new responsible lending regulations.

National has drafted legislation it says could undo the damage new responsible lending regulations have done to borrowers’ chances of getting a home loan.

National Housing spokeswoman Nicola Willis said she had written to Trade and Consumer Affairs Minister David Clark asking him to pass Andrew’s private member’s bill as a matter of urgency. Bayly.

Critics of the new regulations, which came into force on December 1, say they are too prescriptive and mean that some people are no longer eligible for bank mortgages that would have been given to them previously.

Willis said: “Regulations have led banks to intrusively audit the spending histories of potential borrowers and Kiwis have had their loan applications rejected for absurd reasons like buying takeout too often, subscribing to Netflix or go to therapy.”

READ MORE:

* SBA boss is confident tough new lending rules will be eased so fewer home loan seekers are ‘weeded out’

* Lending slowdown: government tricks or lenders crying wolf?

* Banks deny minister’s accusation of irresponsible lending

She said the regulations were meant to target predatory and high-risk lenders, not force heavily regulated banks to cut their mortgages.

Bayly’s bill would change the regulatory powers of the Credit Agreement and Consumer Finance Act to allow for different regulations for different types of lenders.

This would allow for stricter and more prescriptive responsible lending rules for lower-tier lenders like payday lenders, while leaving banks less regulated.

RYAN ANDERSON

Independent economist Tony Alexander says mortgage lenders’ willingness to lend has declined.

“The government has taken a comprehensive approach that subjects banks to the same set of highly prescriptive and draconian regulations as high-risk payday lenders, although banks are already subject to a comprehensive set of mortgage standards enforced by the Bank. spare,” Willis said.

“There is a categorical difference between regulated financial institutions that issue long-term mortgages at low interest rates and other types of higher-risk, shorter-term loans issued by other lenders at different purposes,” Willis said.

The bill would require the minister to consider their different scale and risk profiles when setting regulations for their lending business.

“We want to work with the government to pass this law. This is an immediate problem with the hopes and financial futures of thousands of Kiwis at stake. We urge the government to give our proposal proper consideration,” she said.

Bayly’s bill is called the Consumer Credit Agreement and Financing Amendment Bill (Reasonable Investigations by Regulated Financial Institutions).

ROBERT KITCHIN/Stuff

National’s commerce spokesman Andrew Bayly has drafted legislation he says could preserve defenses against predatory lenders, without preventing banks from extending home loans to non-vulnerable borrowers.

Following face-to-face meetings with Clark last week, the chief executives of ANZ and ASB made public statements about the proportion of home loan applications their banks have had to turn down since December 1, which that they would have previously approved.

ANZ’s Antonia Watson said it was six out of 100 loans, while ASB’s Vittoria Shortt said it was seven out of 100.

Our goal at Credible Operations, Inc., NMLS Number 1681276, hereafter referred to as “Credible”, is to give you the tools and confidence you need to improve your finances. Although we promote the products of our partner lenders who pay us for our services, all opinions are our own. Taking out a bill consolidation loan can […]]]>

Our goal at Credible Operations, Inc., NMLS Number 1681276, hereafter referred to as “Credible”, is to give you the tools and confidence you need to improve your finances. Although we promote the products of our partner lenders who pay us for our services, all opinions are our own. Taking out a bill consolidation loan can […]]]>Our goal at Credible Operations, Inc., NMLS Number 1681276, hereafter referred to as “Credible”, is to give you the tools and confidence you need to improve your finances. Although we promote the products of our partner lenders who pay us for our services, all opinions are our own.

Taking out a bill consolidation loan can make it easier to manage your bills and potentially lower your monthly expenses. Learn more. (Shutterstock)

If you’re having trouble coping with multiple debts, bill consolidation could be a solution. Bill consolidation is the process of combining multiple bills (like medical bills and credit card bills) into one debt by taking out a new loan.

A personal loan to consolidate your bills could help you get a lower interest rate if you’re burdened with high-interest debt. But before applying for this type of loan, you should consider all the pros and cons.

What is an Invoice Consolidation Loan?

A bill consolidation loan, also known as a debt consolidation loan, is a personal loan that you use to pay off your existing debt. If you are approved for one, a lender will give you a lump sum that you can then use to pay your bills. Or, the lender can use the funds to pay your creditors directly. Then you will start making payments on the new loan with one monthly payment.

Some benefits of taking out a debt consolidation loan include reducing the number of bills you have to keep track of and potentially reducing your interest rate and monthly payment amount. But some lenders may charge an origination fee for processing the loan, which is usually deducted from your loan amount. Before accepting the loan, make sure you fully understand all fees.

When does a bill consolidation loan make sense?

Signing up for bill consolidation could be a good financial decision in the following scenarios:

You want a lower monthly payment

If you’re having trouble keeping up with your monthly payments, loan consolidation can reduce the amount you pay each month. This could be the case if you get a lower interest rate or replace an existing debt with a loan with a longer repayment period. Remember that choosing a longer repayment period will likely mean you’ll pay more interest over time.

You want a single payment

Coping with multiple bill payments can be a challenge. And if you miss a payment, it could lower your credit score and lead to late fees. A bill consolidation loan combines your monthly payments into one. As a result, you may be less likely to make late payments, which could save you money and help avoid damaging your credit.

You want a lower interest rate

If your credit score and finances have improved since you took on debt, you may qualify for a lower interest rate with a bill consolidation loan. This could help you save money on interest and get out of debt much faster, especially if you’re consolidating high-interest credit card debt.

How to consolidate your debts with a bill consolidation loan

If taking out a bill consolidation loan is right for you, here’s what you should do to consolidate your debt:

- Make a list of your debts. Create a list of all the debts you want to consolidate. Add the total to find out exactly how much you need to borrow.

- Compare lenders. Research and compare different lenders. This will help you find the lowest rates and the best option for your situation.

- Get prequalified. Prequalify with as many lenders as possible to get an idea of the rates and terms you could receive if approved.

- Choose the best loan for you. Once you’ve compared several loan options, choose the best lender for your situation.

- Submit a loan application. After choosing a lender, submit an official loan application. The lender will look at your credit score, income, debt-to-income ratio (DTI), and other key factors to determine if you qualify.

- Receive your loan funds. If you are approved for a loan, your loan funds are usually deposited into your account after you sign your loan agreement. This usually takes one to seven business days, depending on the lender.

- Pay off your debts. Use the loan funds to pay off the debts you want to consolidate, if your lender doesn’t pay your debts directly.

- Make payments on your bill consolidation loan. Repay your loan as agreed – remember to make payments on time to avoid possible late fees. Sign up for automatic payment, if possible, or use a bill management app to find out when your payment is due.

What to consider when choosing a lender

When shopping for a personal loan, it’s important to compare lenders and rates. This helps you find the best deal available. Here are some things to consider when doing comparison shopping:

- Annual percentage rate – The APR of your loan takes into account your interest rate plus any fees. This is an important number because it helps you understand the true cost of the loan.

- Costs – Origination fees, late fees, and prepayment penalties are all common types of personal loan fees. If possible, choose a lender that has no origination fees so that any funds you receive are used to consolidate your debts.

- It’s time to finance — Consider how long you will need the loan funds. Some lenders can issue your funds the next business day, but others can take much longer. If you need your money quickly, choose a lender known for its speed of financing.

- Minimum credit score — Different lenders have different minimum credit score requirements. While some lenders will approve borrowers with fair credit, other lenders will require you to have good to excellent credit.

- Advantages of the lender — Many lenders offer additional perks, such as free credit monitoring and tailored monthly payments. These may be a factor in your decision.

Bill Consolidation Loan FAQs

What types of debt can I consolidate?

You can use your loan funds to consolidate several types of debt, such as credit card bills, utility bills, payday loans, and more. But before taking out a debt consolidation loan, check with the lender if they have any usage restrictions for borrowers. Some lenders may prohibit you from using personal loan funds to repay a student loan.

Should I consolidate all my debts?

You are allowed to choose which debts you want to incorporate into a debt consolidation loan. Consolidating all your debts may not be possible depending on the loan amount you receive. Also, consolidating certain debts may not make sense if it results in a higher interest rate.

Does debt consolidation hurt my credit rating?

Bill Consolidation Loan Alternatives

When it comes to simplifying your bills and potentially lowering your interest rate, a The debt consolidation loan is not your only option. Here are some alternatives to consider.

Balance transfer credit card

Looking to consolidate your credit card debt? A balance transfer credit card lets you transfer a balance from one credit card to another, and many offer an introductory interest rate of 0% or low for a certain period of time.

By taking advantage of one of these offers, you could save a lot of money on interest. The downside is that once the promotional period expires, you’ll have to pay the standard credit card interest rate on any remaining balance. Additionally, you may have to pay a balance transfer fee, which typically ranges from 3% to 5% of the transfer amount.

Student Loan Refinance

If you have student loans and want to consolidate them, student loan refinancing is probably a better option than a bill consolidation loan. When you refinance your student loans, you take out a private student loan to pay off your existing federal or private student loans.

If you have good credit and a decent income, you may qualify for a lower interest rate. The downside is that if you refinance your federal student loans, you will lose access to federal benefits, such as income-based and forbearance repayment plans.

The debt avalanche method

If you don’t want to consolidate or refinance your debt, you can use a debt repayment strategy to effectively eliminate your debt.

With the debt avalanche method, you first pay off your debt at the highest interest rate. You are putting any extra money you have on this debt while making the minimum payments on your other debts. Once that debt is paid off, you move on to the debt with the next highest interest rate.

One advantage of this method is that it helps you save the most interest. But it might take you a long time to pay off your debt with the highest interest rate if it is a large amount.

The Debt Snowball Method

The debt snowball method is another popular method you can use. With this repayment strategy, you pay off your debt with the smallest balance first. This means investing any extra money in this debt while making the minimum monthly payments on your other debts. Once that debt is eliminated, you move on to paying off the debt with the next smaller balance.

One of the main advantages of the snowball method is that you will eliminate your small debts more quickly. When you see this progress, it can motivate you to keep reducing your debt. But the downside is that you might pay more interest with this strategy because your high-interest debts might not be the first ones you focus on.

Home equity loan or home equity line of credit

If you’re a homeowner, you may be able to tap into the equity in your home by taking out a home equity loan or a home equity line of credit (HELOC).

Since these loans are secured by your home, they may come with lower interest rates than you would get with an unsecured personal loan. But you risk foreclosure on your home if you fail to repay the loan.

In 2019, Shelly-Ann Allan’s bank refused to lend her the money she needed to pay for her father’s funeral, so she had to turn to a payday loan company. But what she didn’t take into account was the death of her stepfather shortly afterwards. She had to take out another payday loan in addition to […]]]>

In 2019, Shelly-Ann Allan’s bank refused to lend her the money she needed to pay for her father’s funeral, so she had to turn to a payday loan company. But what she didn’t take into account was the death of her stepfather shortly afterwards. She had to take out another payday loan in addition to […]]]>In 2019, Shelly-Ann Allan’s bank refused to lend her the money she needed to pay for her father’s funeral, so she had to turn to a payday loan company.

But what she didn’t take into account was the death of her stepfather shortly afterwards. She had to take out another payday loan in addition to the one that still had a balance of $1,500.

“Interest rates [have] built and built on me, and that’s where it’s affecting me right now,” said Allan, who lives near Jane and Finch, an area of the city that has a disproportionate number of payday loan companies.

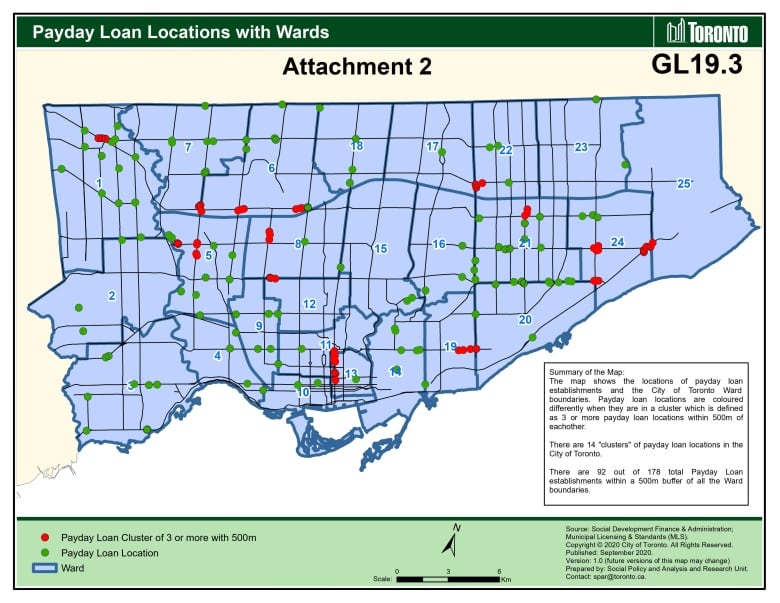

Critics say the concentration of these companies in low-income communities helps perpetuate the cycle of poverty. That’s why Toronto City Council is discussing a recommendation from its housing and planning committee this week that would ban new payday lending establishments from locating within 500 meters of social services offices, public housing, liquor stores, casinos and pawnshops.

According to Allan’s contract with payday loan company easyfinancial, her cumulative interest rate is now 47% and she now owes $24,000. She says people where she lives need more than just zoning restrictions to restrict payday lenders, they also need financial institutions that will lend them money at reasonable interest rates.

“People like me…the bank wouldn’t look at me to lend, because they said I wouldn’t be able to pay that money back,” Allan said.

Zoning boundaries

Currently, lenders in Ontario cannot charge more than $15 in interest for every $100 borrowed.

Despite this, Andreas Park, a professor of finance at the University of Toronto, says annual percentage rates can reach over 400% for short-term payday loans, and additional interest can be charged if the loan fails. is not repaid at the end of the term, according to the Payday Loans Act.

A 2021 report by city staff indicates that the zoning restrictions would only apply to new establishments and could not apply retroactively to existing establishments.

In 2018, the city capped the number of payday loan licenses and locations. The city says this contributed to a decrease of more than 20% of these establishments, from 212 to 165 as of January 26. But a new supplementary report released days before the city council meeting this week shows that the remaining movements of payday outlets have been limited, with only three movements since the city introduced these restrictions.

Staff recommended finding “improvements in consumer protection and access to low-cost financial services” as a way to regulate the industry.

Com. Anthony Perruzza, who represents Ward 7, Humber River-Black Creek, says it’s all part of the city’s Poverty Reduction Initiative.

“But that plan is still being worked on, and there are still a few years to work out.”

Park says zoning restrictions against businesses are limited in their ability to get to the heart of the problem.

“It’s quite striking that these payday lenders are so prevalent in poor neighborhoods and there isn’t a better service on offer,” said Park, who agrees that vulnerable groups need better access to loans at reasonable interest rates.

“Why haven’t we put systems in place that help them overcome some of the challenges they face? »

ACORN Toronto, an advocacy organization for low- and middle-income groups, says that while it welcomes the reduction in payday loan points, the city should follow Ottawa and Hamilton, who have already put restrictions in place. zoning.

“The more frequently residents see these businesses, the more likely they are to consider accessing the high compound interest loans,” wrote Donna Borden, director of East York ACORN, in a letter to the city.

“We think it’s not about planning logic, but about equity, human rights and fair banking.”

The City needs federal and provincial help

The last time the council discussed this topic was in December 2020, where it made numerous requests to the federal government to strengthen enforcement against predatory lending and to the province to provide options for cheaper loans to consumers.

The Ontario government told CBC News it is considering feedback from a 2021 consultation with stakeholders and the public on ways to address the issue.

Additionally, the Federal Department of Finance said in an emailed statement that the government is considering cracking down on predatory lenders by lowering the criminal interest rate, which is now set at 60%. However, payday lenders are exempt from this provision in provinces that have their own financial regulatory system, such as Ontario.

Perruzza says these lenders are predatory and need to be regulated at all levels of government, especially in the wake of COVID-19.

“We really need to impress upon the federal and provincial governments that this is a huge problem and that they need to use their legislative tools at their disposal.”

A truck heads east along historic Route 66 in Albuquerque in this 2017 photo, past a sign advertising a securities lending business. New Mexico lawmakers are considering lowering the current 175% state cap on small loan interest rates during this year’s 30-day legislative session. (AP Photo/Susan Montoya Bryan) SANTA FE — It may seem like […]]]>

A truck heads east along historic Route 66 in Albuquerque in this 2017 photo, past a sign advertising a securities lending business. New Mexico lawmakers are considering lowering the current 175% state cap on small loan interest rates during this year’s 30-day legislative session. (AP Photo/Susan Montoya Bryan) SANTA FE — It may seem like […]]]>SANTA FE — It may seem like déjà vu at the Roadhouse, but a bill dealing with how New Mexico limits interest rates on storefront loans is on the way again.

A year after a similar measure died in a standoff between House and Senate members, a new proposal lowering the annual cap on interest rates on small loans — from 175% to 36% — has passed Saturday by its first House committee.

“It’s truly a financial epidemic,” said Rep. Susan Herrera, D-Embudo, who said more than 20 percent of residents have taken out such loans in about half of New Mexico’s counties.

She also said out-of-state companies have moved into New Mexico to take advantage of low-income residents who need quick access to cash.

However, just like last year, critics of the legislation argued that lowering the state cap on interest-rate loans could put businesses out of business and leave their employees unemployed.

They have argued in the past that such a policy change would push borrowers to use internet lenders, many of which are based in other countries and cannot be regulated.

Danielle Fagre Arlowe of the American Financial Services Association, a Washington DC-based group, said the bill would make it harder for people with bad credit to get loans.

“Low-income residents will likely find themselves in credit deserts if (this bill) passes,” she told members of the House Consumer Affairs and Public Affairs Committee.

But the committee ultimately voted 3-2 to approve the measure, with Democrats voting in favor and Republicans voting against.

This year’s legislation, House Bill 132, is sponsored by a bipartisan group of five lawmakers, including House Speaker Brian Egolf, D-Santa Fe. It would lower the state’s interest rate cap on loans showcase, but would also increase the maximum amount of these loans from $5,000 to $10,000.

In its original form, the bill also included a $180,000 credit for financial education efforts in New Mexico schools, but that was removed from the legislation Saturday at Herrera’s request.

Under current state law, proponents of the bill said storefront loan companies currently target the state’s Native American population and low-income areas.

Additionally, a December survey of Latinos in New Mexico found that 19% of adults had taken out a storefront loan during the COVID-19 pandemic.

“People say it helps – it doesn’t help,” said Leonard Gorman, executive director of the Navajo Nation Human Rights Commission, who described current interest rates on many small loans as “harmful” to those who have trouble repaying them.

New Mexico has a long history of regulating the lending industry.

A previous 36% cap on loan interest rates was abolished by the Legislature in the 1980s amid high inflation, according to research by Santa Fe-based Think New Mexico, which has is pushing for the lower rate cap to be reinstated.

After years of Roundhouse debate, lawmakers passed a 2017 bill that established the current 175% interest rate cap on small loans and banned so-called payday loans with terms of less than 120 days.

But critics have insisted that the 175% cap can leave low-income New Mexicans stuck in “debt traps,” while pointing out that the US armed forces have implemented an annual rate limit in 36% percentage for loans obtained by active duty military personnel.

The Roundhouse debate has caught the attention of many national businesses who have hired lobbyists to represent their interests.

During last year’s legislative session, a credit industry lobbyist said the industry employs about 1,300 people across New Mexico.

Additionally, small loan companies made $140,000 in campaign contributions to New Mexico candidates and political committees during the 2020 election cycle, according to a recent report by New Mexico Ethics Watch.

The bill to cap interest rates on loans is now before the House Judiciary Committee with less than three weeks remaining in this year’s 30-day legislative session.

Sponsored content A small loan is a type of unsecured loan. This means you don’t have to post collateral in case you don’t repay your existing loan. The lender does not have the right to confiscate your property if you take out a small loan and do not repay it on time. Nevertheless, there are […]]]>

Sponsored content A small loan is a type of unsecured loan. This means you don’t have to post collateral in case you don’t repay your existing loan. The lender does not have the right to confiscate your property if you take out a small loan and do not repay it on time. Nevertheless, there are […]]]>Sponsored content

A small loan is a type of unsecured loan. This means you don’t have to post collateral in case you don’t repay your existing loan. The lender does not have the right to confiscate your property if you take out a small loan and do not repay it on time. Nevertheless, there are negative consequences: your credit rating will drop and your small loan could be declared in default.

Small loans require collateral such as your home in the case of a mortgage or your car in the case of a car loan. Small loans use your credit score and credit history to determine if you qualify.

Small loans generally do not have strict requirements. Instead, you can use a small loan for almost anything as long as it initially meets the conditions set out in your loan agreement, you can also learn more about MoneyZap, one of the organizations that offer small loans. Small loans are given as a lump sum and you make monthly payments until your loan is paid off in full. As long as you make your monthly payments, you continue to spend what you want within your limit.

Reasons for taking out a small loan

Small loans or personal loans can be used for almost all your needs within reason and in accordance with the terms of your loan. You cannot use the money for anything illegal. In most cases, for the cost of post-secondary education. Here are some good reasons to get a small loan:

Emergency cash assistance

If you need money right now to cover bills, urgent expenses, or anything else that needs immediate attention, you can take out a small loan. Most lenders provide online applications that let you know if you’ve been approved within minutes. You can get financing the same day or within a few business days, depending on your lender.

You can use the loan to cover emergencies such as:

- Payment of late payments for housing and utilities;

- Medical bills;

- Unscheduled car repairs;

- Funeral expenses.

A small unsecured loan is a good alternative to a payday loan. Payday loans are short-term, high-interest loans that usually have to be repaid when you get your next paycheque. Typically, you won’t need to go through a credit check and you can get financing right away. But payday loans can do more harm than good. Interest rates can reach 400%, and many borrowers do not have the funds to pay off the loan in full as quickly as payday loans require.

Home improvement and renovation

If you own a private home, you can take out a small loan to renovate or modernize it. You can also take out a consumer loan. Home loans and lines of credit are perfect for tackling real estate projects. They are secure and use your home as collateral. If you don’t want to risk losing your home if payments are delayed, a small loan is a reliable substitute in this case. Along with that, getting a small loan can be faster compared to a home equity loan.

Moving expenses

If you move near your current place of residence, you may not have to cover major expenses. If you’re moving out of state, you may need extra money to pay for travel expenses with a personal or home loan. Moving means covering the cost of packing your belongings, possibly hiring movers, and transporting your belongings to a new location. A personal loan will also help fund the process of finding a new home. For example, if you find an apartment, you may have to pay the first month, the last month and a deposit. You may also need money to furnish your new home.

Debt Consolidation

Americans owe $1 trillion on their credit cards. Although some of them include purchases made by people, they include interest and fees. It all adds up and can deter many consumers from paying off their credit card debt. A personal loan can be used as debt consolidation, especially when it comes to credit card debt. This is also a popular reason why people take out a personal loan.

Small loans charge low interest rates compared to credit cards, especially if you have a good credit rating. The best loans charge an interest rate of only 4% lower than the double digit interest rates charged by most credit cards. You can take out a loan, pay off your credit card balance, and then make a one-time payment to your new loan department staff.

Wedding expenses

Financial experts do not recommend borrowing money to pay for a wedding. Instead, consider reducing your wants to stay within your acceptable budget. If you need to borrow money, you have several options such as credit cards and personal loans. Credit cards have higher interest rates than personal loans. There may be even higher interest rates and fees when dispensing cash by credit card. A small consumer loan is a less expensive borrowing option if you need money to cover major expenses.

Total amount of loan overpayment

Do not complicate your life with independent calculations, multiplying interest by the amount of the loan, adding up commissions, etc. Ask the bank or MFO for an approximate payment schedule from which it is easy to calculate the amount of the overpayment. Banks do not always have their own operational offices in your city to receive loan repayments. Thus, be sure to specify the method of payment through the terminals. Add the commission to the overpayment amount on the schedule. You will receive the absolute amount of the overpayment in dollars for your convenience. You can divide it by the loan amount and get the overpayment in %.

Keep in mind that the actual payment schedule when obtaining a small loan may differ from that provided to you at the pre-consultation stage. Therefore, before signing the loan agreement, check the final payment schedule with the original and the offer competitors. Feel free to get up and go if the loan terms and payment schedule differ from the original ones that suit you.